The hidden value on operation execution for the pulp and paper industry – How big is it and why does it matter?

Pulp and paper companies are facing continuous pressure on their profitability as the markets get more competitive. Our experience tells us that there is a lot of money left on the table that is related solely to the intrinsic operational capability. Capturing this hidden value can make the difference between success and failure.

The main pillars for business success

There are plenty of business management theories that describe why some businesses are successful and others aren’t, but from our point of view, the success of any business relies on three main pillars: strategy, assets and execution.

Clearly, getting the business strategy right is paramount, as it will define the organisation’s direction and development. The basis of this strategy should be defining which products and services provide the most added value, and which geographies offer the best opportunities. This can then be supported by M&A, organic growth or other decisions.

The second pillar of any strategy is the organisation’s assets; in other words the physical equipment in which the products are manufactured. The type of technology, its technical age (new investments versus upgrades) and the level of automation will define the potential competitive edge that the company will have within the industry.

The final element of success is the way the people and organisation execute its strategy with the available assets. For this, adequate operational capability is needed to achieve target profitability in the prevailing market context.

The “asset quality” myth in the pulp and paper industry

In a capital intensive industry like pulp and paper, there is a tendency to believe that asset quality (technology, age and maintenance) is the main determinant factor of operational performance. If everything else is constant, then asset quality determines the competitiveness potential, but assets are just the hardware in an industry that has historically overlooked operational execution. Many pulp and paper mills have old assets but strong operating performance, while others have newer assets but trail on overall efficiency.

In a highly competitive industry, it is the companies that learn how to maximise the value of their assets, regardless of their age, that will achieve a competitive advantage. This can only be achieved with excellent operating practices that focus on process stability, optimisation and continuous improvement. Our experience shows that, by failing to optimise their processes, many organisations are effectively leaving money on the table. Capturing this hidden value is ever more important for the pulp and paper industry due to challenging market conditions, and can be the difference between success and failure.

The pulp and paper sector - a mature and maturing industry

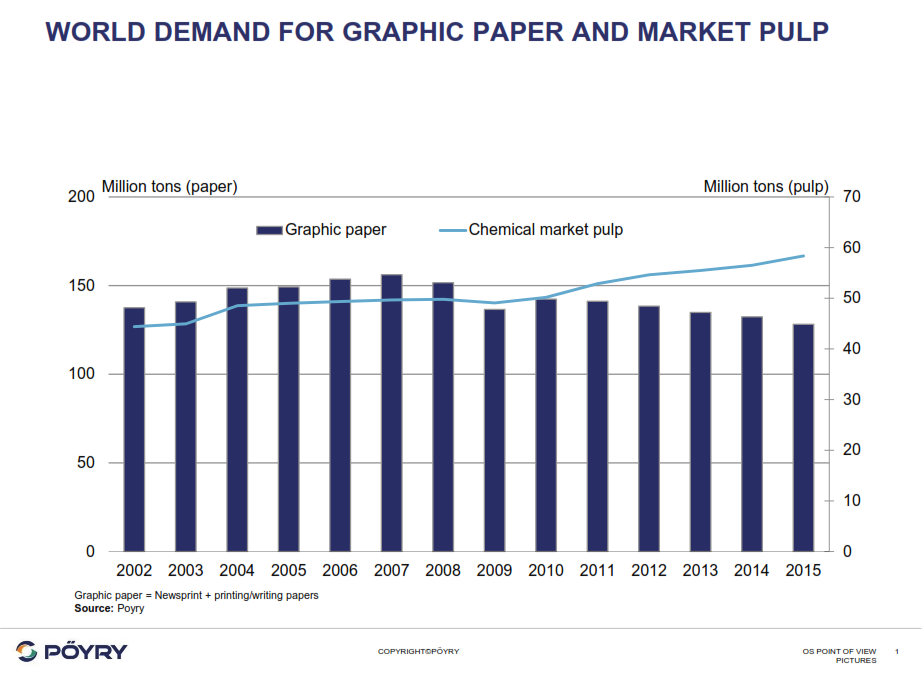

The pulp and paper sector is a mature industry that has very different segments and geographic realities. On the paper side, sales of industrial and hygienic grade papers are still growing globally, but graphic paper sales are declining due to the developed markets sunset. On the pulp side, emergent markets in Latin America have gained the upper hand due to several competitive advantages, related to lower cost base. In fact, this geographic shift from mature, fibre-rich western markets towards emergent markets has been the industry’s guiding force in the 2 decades. In turn, this has led to a gradual shift away from vertically integrated pulp and paper operations, towards a market pulp and recovered paper-driven industry. Also, the decline of non-wood supply in China and the tissue move into virgin fibre have supported virgin pulp markets.

The main result of this shift is that the developed markets will continue to mature, with some segments declining as a result. This will put additional pressure on existing pulp and paper players in Europe and North America, where improving the overall operating performance is now essential.

The tides are more favourable in emerging markets, but investment cycles prove that these markets are also maturing. With this, more focus needs to be given to the operational efficiency of current assets, rather than looking at new investments. The issues are common regardless of geography and the position on the investment cycle.

Pulp and Paper Industry has become a global competitive arena with ever tighter margins

Key market drivers are putting pressure on overall industry profitability

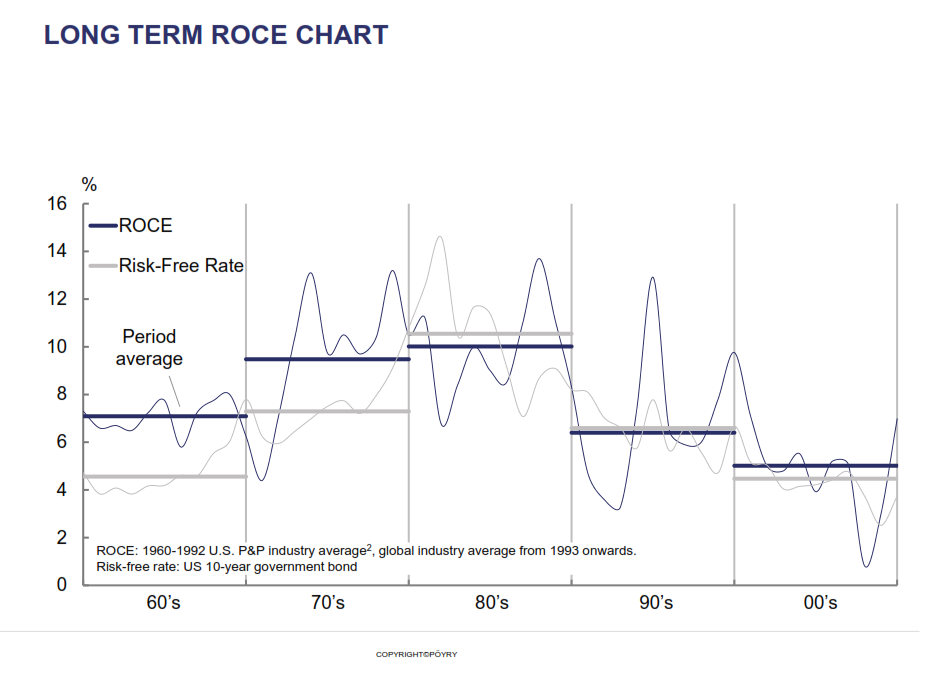

In recent years, pulp and paper producers have endured challenging conditions, resulting in unsatisfactory profitability. Although profitability varies from segment to segment, generally speaking this poor performance has been driven by poor capacity utilisation, declining demand, a low level of supplier concentration, poor sales prices and unfavourable exchange rates. The markets are complex, and the drivers vary from one industry sector to another and over time.

Profit margins are influenced by a number of factors but typically market forces cannot be controlled by companies. This means improving sales and reducing overall costs is necessary in a highly competitive environment.

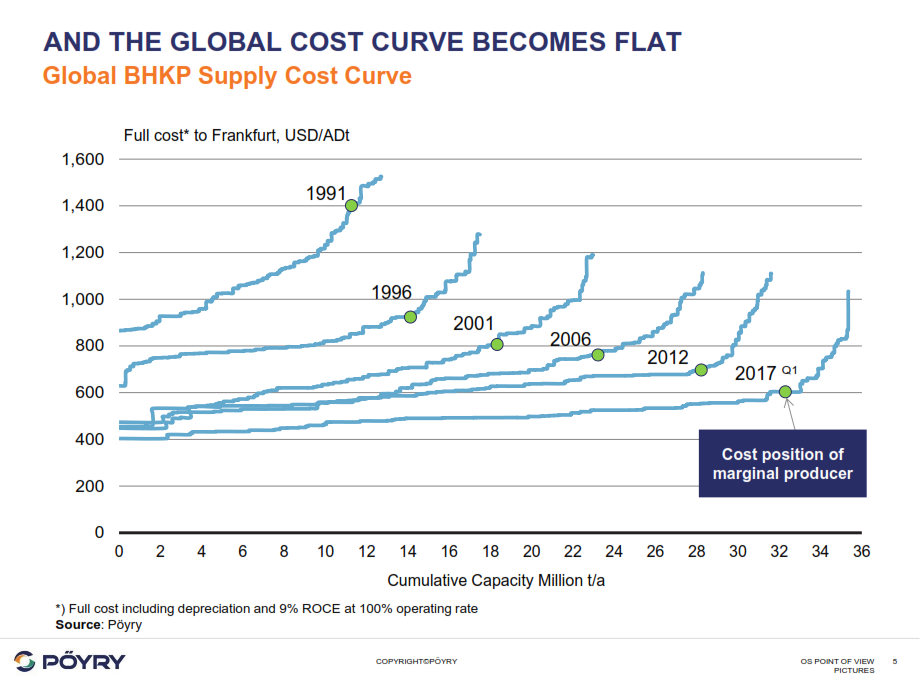

The pulp and paper industry has evolved into a highly competitive global arena where producers have positioned themselves on the lowest cost position possible while capturing relevant market shares.

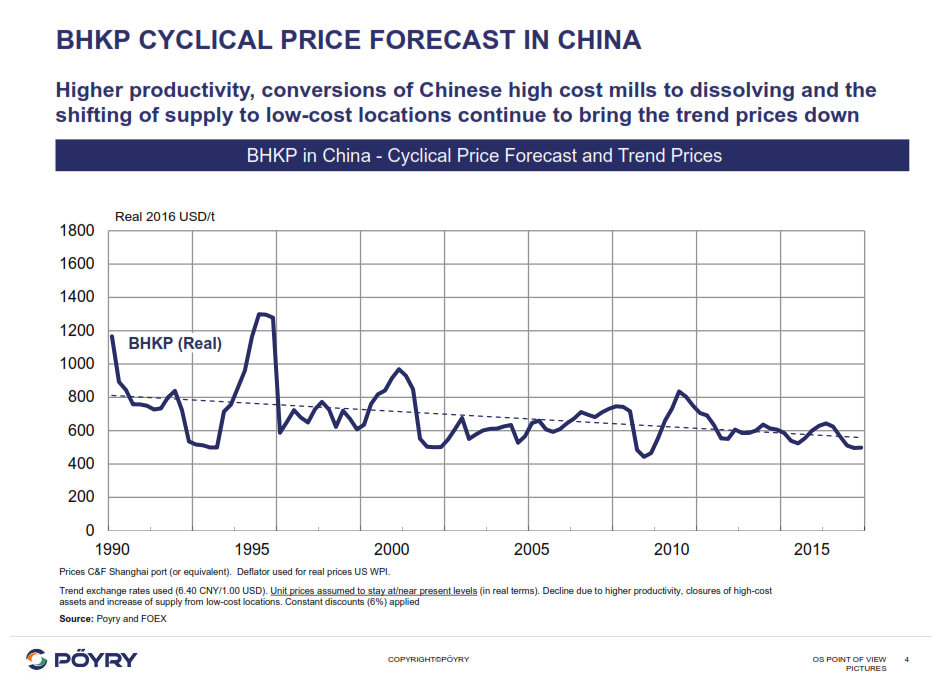

To illustrate this, the recent additional BHKP capacity responding to higher demand has positioned the new producers at the lower cost end. Production costs have declined as a result of highly-competitive raw material prices, growing economies of scale and declining transport costs, in turn forcing high- costs producers out of the market. As a consequence, the flattening BHKP market pulp supply curve increases competition for profitability, punishes inefficient producers and exposes players to price fluctuations.

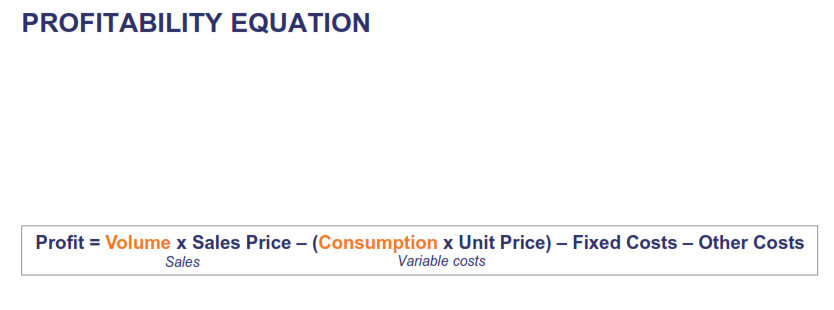

In this context, companies have low degrees of freedom to affect the Sales Price Profitability Lever as this is fundamentally the result of market balance. To compensate for this reduced profitability that affects most of the pulp and paper grades, companies have looked at rationalising their production costs to keep profitability at acceptable levels. This might include consolidating the business, streamlining operations and reducing their overheads (including their number of FTEs). However cost- cutting can only do a limited amount for increasing profitability.

By necessity the next step must be improving operational efficiency, which is the lever that the company can actively control. Ultimately, this can positively impact production volumes or raw materials and utilities consumption, which has direct effect on the profit equation, regardless of market conditions.

Focus on what you can control - Execution Gap

Main internal levers for operations performance

Improving operational performance and efficiency is not straightforward. Plenty of companies find themselves unable to achieve significant improvements even though they expend significant resources on it. While continuous improvement initiatives have been a part of business culture for a long time, the pulp and paper sector has always been somewhat conservative in making it a common management practice.

When companies do apply continuous improvement initiatives, they often find they do not have the right operational capability to develop and implement effective and consistent performance improvement initiatives and harvest visible results.

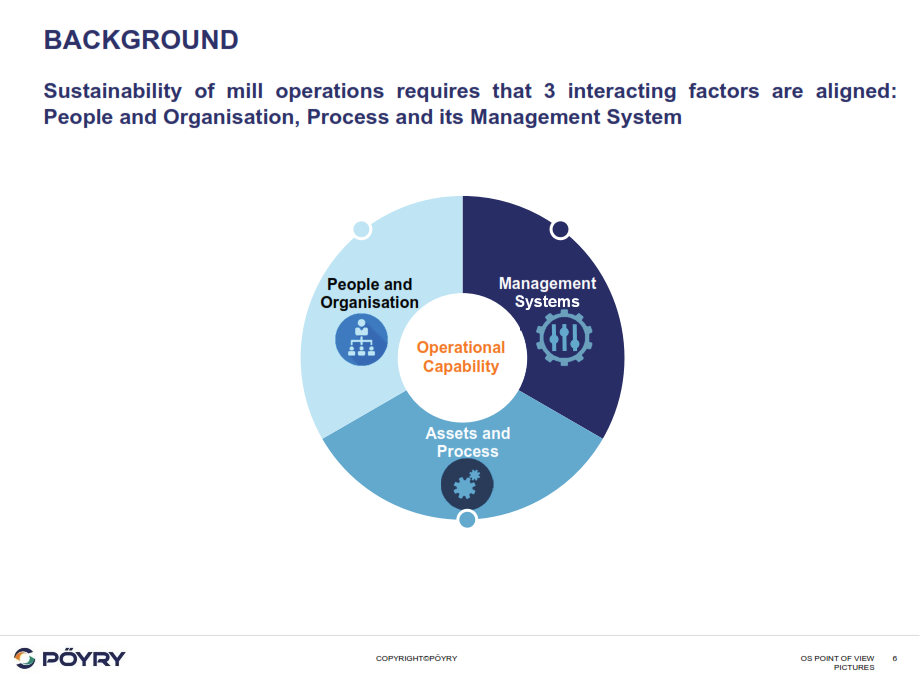

Operations performance can be determined by the quality of three main factors: assets and process, people and organisation, and management systems.

- 1. Assets and processes – this is the way physical assets are run and optimised to create value, while minimising losses through improved stability. It is related to the design of manufacturing and business process, as well as to the subsequent ability to technically improve the business and physical proc

- 2. People and organisation – this is the way people organise, think, perform and conduct themselves in the workplace, both individually and collectively. It is related to the organisational structure, as well as people’s skillsets that can support the goals of an effective continuous improvement culture.

- 3. Management systems – this is the formal structure, processes and systems through which human and organisational resources are aligned to achieve shared go It can include elements such as process variable tool monitoring, KPI reporting, shift reports, action planning systems and standard operating procedures. These systems should be geared towards effective continuous improvement.

These levers can be used in a number of different ways to improve operations, but they all aim to change operating methods and procedures together with the use of modern technology in operational control. Several companies have applied different methods such as Lean Six Sigma, Lean Management, TPS, Kaizen and Deming’s Circle – PDCA. But, understanding the technical challenges of the pulp and paper industry when applying continuous improvement tools is key, as out of- context implementation can actually do more harm than good.

Having recognised this, Pöyry has developed a methodology that incorporates the best of different continuous improvement techniques, while bringing industry savvy experts that can understand the specific needs of pulp and paper mills and speak their language. Pöyry’s ExGapTM methodology is based on sound analytics and process insights into operations, supply chain and organisation.

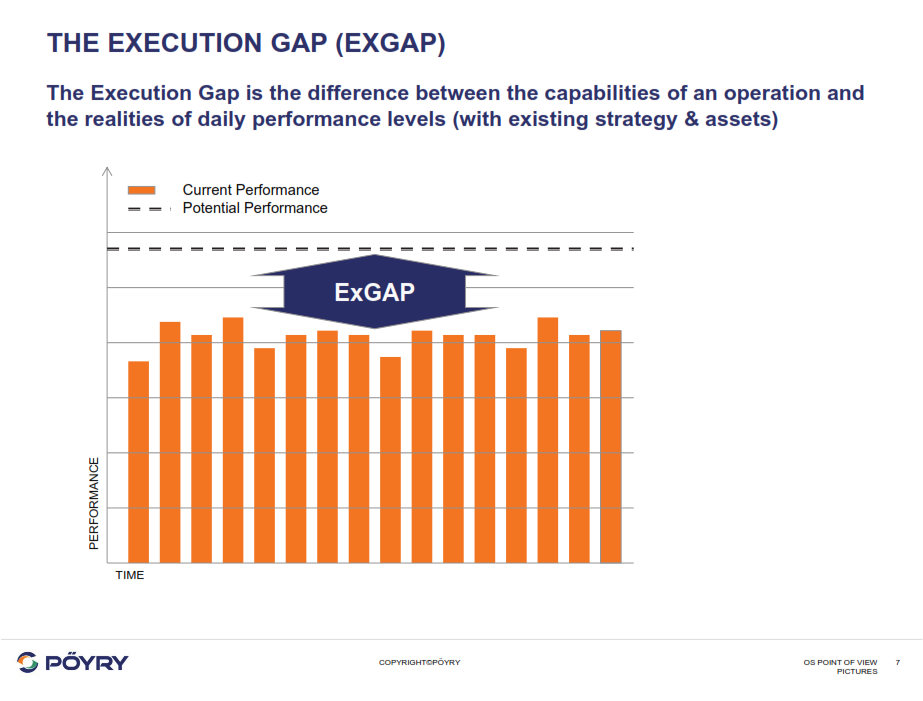

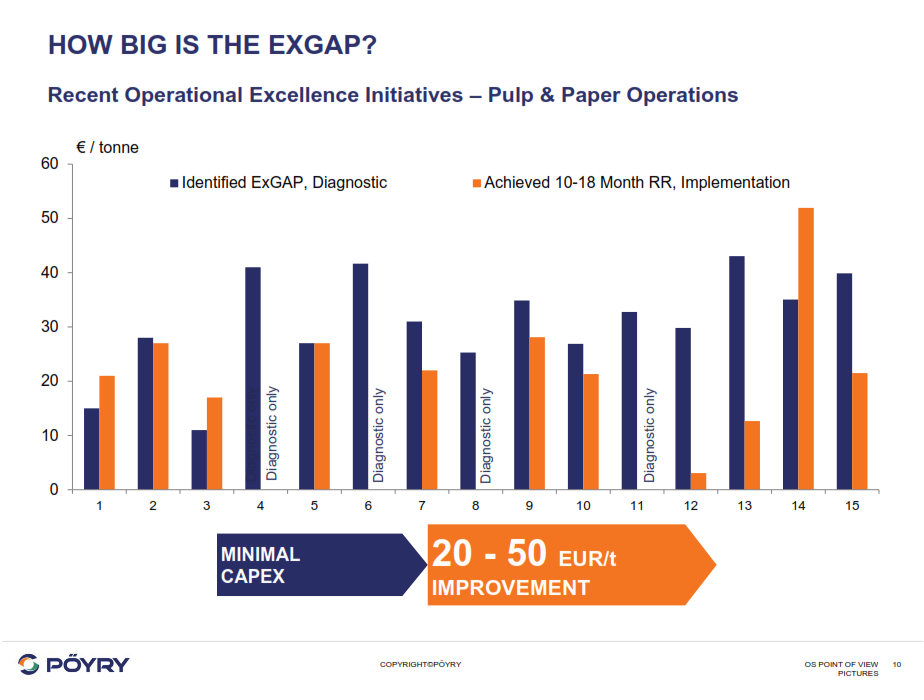

Execution Gap – how much value are we leaving on the table?

Fundamental to Pöyry’s ExGapTM methodology is qualifying and quantifying the Execution Gap (ExGap) of an operation. This can be defined as the difference between current performance and potential performance. It is the money that companies are leaving on the table by not being able to perform to their full potential with their current assets. This is a simple but powerful concept that is the first step on the long path towards sustainable performance improvement. Though a simple concept, the ExGap contains a powerful message:

- It is usually significant – all industries, all market conditions

- It is within our control

• It will never be captured until it is specifically identified and quantified

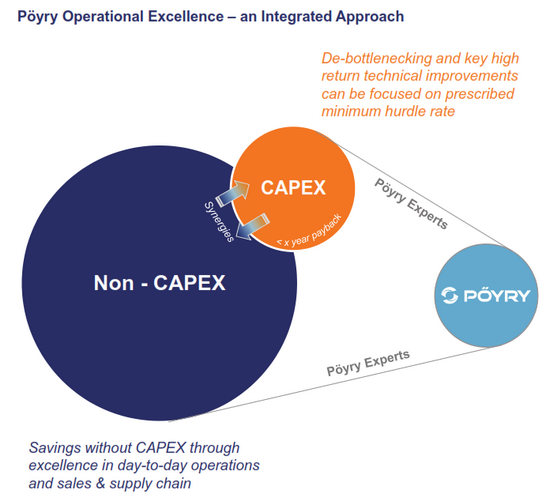

The first step towards establishing and quantifying the ExGap is undertaking a mill diagnostic. This entails a full management process and system diagnostic, together with a technical process diagnostic, combining both management and technical perspectives. The diagnostic focuses mostly on non-capex areas of opportunity, as most of the improvement can come from better process monitoring and control. This highlights how most process improvement is unrelated to asset investment. Nonetheless, in selected circumstances, rapid return investments can also be identified to accelerate the ExGap closure.

Typically, for the pulp and paper industry the ExGap on operations can reach between 20-50EUR/t of improvement opportunity. Roughly 55% is attributed to increased production (if it can be valued) and 45% is related to variable cost savings. This is a sizeable gap that has a high impact on the bottom-line and can make the difference between a company’s success and failure.

The Pulp and Paper players are facing common challenges preventing them of capturing the full value of their operations

Case Study - Taking operational improvements to the next level

- The client was a recycled graphic paper producer with modern assets who had already executed several improvement initiatives. Their goal was to improve production efficiency and stability. In addition to the technical issues in both paper machines and recycled plant, the mill had structural problems related to its management systems, hindering its performance.

- Pöyry’s team stepped in to conduct an ExGapTM diagnostic with detailed data analysis and technical interviews during a two week site visit. The team identified 20EUR/t of lost productivity in production areas OEE, raw materials and energy consumption. The low performance was clearly attributable to more than mere asset quality: for example, management systems for the production monitoring and control were inadequate. Other typical organisational shortcomings included management of departmental silos, as well as lack of diligent planning, action and accountability.

- The diagnostic phase was crucial to guide the next step on the performance improvement process. Next, Pöyry’s team and the client started to jointly bridge the execution gap, based on the first phase findings. The 12-month implementation project that followed included several changes in management and technical improvement initiatives. These were geared towards developing management system methods and tools for consistency of behaviour, actions and, ultimately, performance and results.

- Importantly, performance transparency was also established. This included visual means and regular reports, clear and manageable targets, as well as improved communication/information sharing through meetings at the mill and within department levels. Emphasis was put on diligence and actions were taken against negligent or unintentionally faulty work. Ultimately, motivation and team mentality improved due to increased accountability.

- By the end of the project, the mill achieved an annualized improvement level of about 4 MEUR on all aspects of the operation. The performance continued to rise further following the establishment of high performance culture. The main achievements included the following: 1) Technical downtime reduced by almost 50% on main PM’s; 2) Increased speed machine by 3%; 3) Break frequency was almost halved on one machine and stabilised on the second machine even with higher speeds; 4) Power consumption reduction of about 10%t; 5) Steam consumption reduction of about 10%.

What are the main challenges that industry faces in operations?

The root of an organisation’s ExGap lies in the three above-mentioned components of operations management – management systems, assets and process, and people and organisation. Issues and challenges that contribute to a company’s ExGap include:

Process variance and inconsistent results – inefficient use of assets together with lack of optimisation and limited standard operating procedures can lead to excessive process variability. Process variability leads to lower efficiencies and higher production costs.

Non-systematic management processes – incomplete or inconsistent management systems are a common cause of poor performance. This can be reflected in poor and incomplete management and process metrics, excessive and unfocused reporting, poor meeting and action structures, informal action planning, or the lack of a formal continuous improvement system. It’s typical to see different departments on the same mill using a different management process and tools.

Poor equipment availability due to sub-optimal maintenance practice – The ineffectiveness of maintenance function is more of an issue than the maintenance costs. Incomplete business processes and lack of management systems tend to generate low visibility and accountability of maintenance results, which reflects on poor equipment availability.

Lack of specific operational and industry skills – as a result of low industry profitability, investment in assets and people has been reduced. This results in a shortage of management and technical skills, which is exacerbated by an ageing workforce.

Obsolete instrumentation and automation – to maintain steady and stable processes, having the correct and most reliable measurements is essential. It is not possible to control a complex process of high inertia with infrequent lab measurements. At the same time, manually operated operations are fallible and prone to variability. Systems obsolescence is becoming a common issue in the pulp and paper industry.

Organisation silos and data overload – mill departments tend to be organised in silos where data and information doesn’t flow across borders. Holistic mill optimisation is thus more difficult. On top of this, pulp and paper mills are overloaded with too much data, and have insufficient time and tools to extract any valuable information or insights.

This is not a comprehensive breakdown of all the challenges the industry is facing, which varies between companies, segments and geographies. Rather, the challenges outlined above are consistently found across the pulp and paper industry and are the main causes of low operational performance.

What are the requirements to improve on operations?

Improving mill operations and achieving performance gains is not straightforward; different companies will have different levels of readiness for the long and sometimes difficult journey required. Ultimately, continuous improvement processes are about fundamental changes to a company’s culture.

There are two phases within Pöyry’s ExGapTM principles that drive continuous improvement processes: firstly, the diagnostic phase and secondly, the implementation phase.

The diagnostic phase is an intensive audit of the company’s operations, with the objective of identifying and quantifying the extent of the opportunities for improvement (ExGap), while also revealing clues about the causes of underperformance. This is a fundamental step, which any improvement initiative should start with. Typically, this can be developed within 1-2 months of intensive work, depending on the areas involved and the complexity of operation.

After diagnosing the state of operations, the next phase involves the implementation of new methods and practices that can help close the ExGapTM. This should be based on a 10-18 month initiative, in which all levels of the organisation are involved. Systematic processes are developed with a clear management structure that helps to unlock the operation’s true potential. At the same time, the development of people is promoted alongside efforts to change company culture. The result is a new approach and new system that is focused on continuous improvement.

In our experience, applying operational excellence methodologies is not enough to achieve tangible results in improving operations in the pulp and paper industry. It must be accompanied by deep technical knowledge of the industry and extensive technological expertise in order to challenge and change deep-rooted operating methods. The path to improvement can be both long and challenging, and companies must fully commit and dedicate all required resources to these initiatives. However, the reward is on the horizon and can be tangible.

Concluding – why all of this matters?

Given the cut-throat competition in the pulp and paper sector, it is imperative that producers extract the most out of their assets. There is typically a great deal of value hidden within underperforming operations. This money is left on the table by companies that are not able to capitalise the best of their operations.

These improvements should be a priority, as they are entirely within a company’s control. Companies can’t control market forces, so focusing on what they can control is essential, and can be the difference between survival and failure. Based on our experience, the potential benefits on production, maintenance and supply chain can yield savings as much as 20-50EUR/t. It is time for pulp and paper companies to claim back this hidden value – the ExGapTM.